The Inflation Reduction Act, signed into law on August 16, 2022, includes health-care and energy-related provisions, a new corporate alternative minimum tax, and an excise tax on certain corporate stock buybacks. Additional funding is also provided to the IRS. Some significant provisions in the Act are discussed below.

Medicare

The legislation authorizes the Department of Health and Human Services to negotiate Medicare prices for certain high-priced, single-source drugs. However, only 10 of the most expensive drugs will be chosen initially, and the negotiated prices will not take effect until 2026. For each of the following years, more negotiated drugs will be added.

Starting in 2025, a $2,000 annual cap (adjusted for inflation) will apply to out-of-pocket costs for Medicare Part D prescription drugs.

Starting in 2023, deductibles will not apply to covered insulin products under Medicare Part D or under Part B for insulin furnished through durable medical equipment. Also, the applicable copayment amount for covered insulin products will be capped at $35 for a one-month supply.

Health Insurance

Starting in 2023, a high-deductible health plan can provide that the deductible does not apply to selected insulin products.

Affordable Care Act subsidies (scheduled to expire at the end of 2022) that improved affordability and reduced health insurance premiums have been extended through 2025. Indexing of percentage contribution rates used in determining a taxpayer’s required share of premiums is delayed until after 2025, preventing more significant premium increases. Additionally, those with household incomes higher than 400% of the federal poverty line remain eligible for the premium tax credit through 2025.

Energy-Related Tax Credits

Many current energy-related tax credits have been modified and extended, and a few new credits have been added. Many of the credits are available to businesses, and others are available to individuals. The following two credits are substantial revisions and extensions of an existing tax credit for electric vehicles.

Starting in 2023, a tax credit of up to $7,500 is available for the purchase of new clean electric vehicles meeting certain requirements. The credit is not available for vehicles with a manufacturer’s suggested retail price higher than $80,000 for sports utility vehicles and pickups, $55,000 for other vehicles. The credit is not available if the modified adjusted gross income (MAGI) of the purchaser exceeds $150,000 ($300,000 for joint filers and surviving spouses, $225,000 for heads of household). Starting in 2024, an individual can elect to transfer the credit to the dealer as payment for the vehicle.

Similarly, a tax credit of up to $4,000 is available for the purchase of certain previously owned clean electric vehicles from a dealer. The credit is not available for vehicles with a sales price exceeding $25,000. The credit is not available if the purchaser’s MAGI exceeds $75,000 ($150,000 for joint filers and surviving spouses, $75,000 for heads of household). An individual can elect to transfer the credit to the dealer as payment for the vehicle.

Corporate Alternative Minimum Tax

For taxable years beginning after December 31, 2022, a new 15% alternative minimum tax (AMT) will apply to corporations (other than an S corporation, regulated investment company, or a real estate investment trust) with an average annual adjusted financial statement income in excess of $1 billion.

Adjusted financial statement income means the net income or loss of the taxpayer set forth in the corporation’s financial statement (often referred to as book income), with certain adjustments. If regular tax exceeds the tentative AMT, the excess amount can be carried forward as a credit against the AMT in future years.

Excise Tax on Repurchase of Stock

For corporate stock repurchases after December 31, 2022, a new 1% excise tax will be imposed on the value of a covered corporation’s stock repurchases during the taxable year.

A covered corporation means any domestic corporation whose stock is traded on an established securities market. However, the excise tax does not apply: (1) to a repurchase that is part of a nontaxable reorganization, (2) with respect to certain contributions of stock to an employer-sponsored retirement plan or employee stock ownership plan, (3) if the total value of stock repurchased during the year does not exceed $1 million, (4) to a repurchase by a securities dealer in the ordinary course of business, (5) to repurchases by a regulated investment company or a real estate investment trust, or (6) to the extent the repurchase is treated as a dividend for income tax purposes.

Increased Funding for the IRS

Substantial additional funds are provided to the IRS to help fund operations and business systems modernization and to improve enforcement of tax laws.

IMPORTANT DISCLOSURES

Altum Wealth Advisors does not provide investment, tax, or legal advice via this website. The information presented here is not specific to any individual’s personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances. These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.

CIRCULAR 230 NOTICE: To ensure compliance with requirements imposed by the IRS, this notice is to inform you that any tax advice included in this communication, including any attachments, is not intended or written to be used, and cannot be used, for the purpose of avoiding any federal tax penalty or promoting, marketing, or recommending to another party any transaction or matter.

Prepared by Broadridge Investor Communication Solutions, Inc. Copyright 2022.

Prepared for Altum Wealth Advisors

Steven Cliadakis, MBA, CFP®, AIF®, Managing Director, Financial Planner

Miste Cliadakis, CWS®, AIF®, Managing Director, Financial Planner

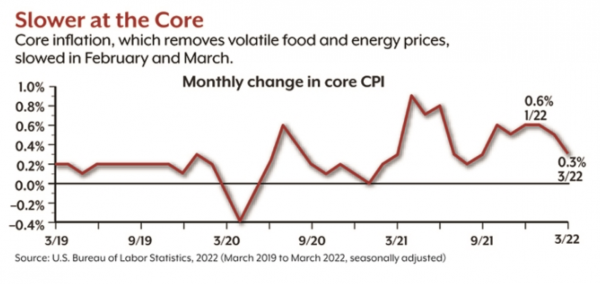

March found that one out of six Americans considers inflation to be the most important problem facing the United States.(2)

March found that one out of six Americans considers inflation to be the most important problem facing the United States.(2) More recently, the Russian invasion of Ukraine has placed upward pressure on already high global fuel and food prices.(3) At the same time, a COVID resurgence in China led to strict lockdowns that have closed factories and tightened already struggling supply chains for Chinese goods. The volume of cargo handled by the port of Shanghai, the world’s busiest port, dropped by an estimated 40% in early April.(4)

More recently, the Russian invasion of Ukraine has placed upward pressure on already high global fuel and food prices.(3) At the same time, a COVID resurgence in China led to strict lockdowns that have closed factories and tightened already struggling supply chains for Chinese goods. The volume of cargo handled by the port of Shanghai, the world’s busiest port, dropped by an estimated 40% in early April.(4)